![]()

Simple bank is an institution with a fine product but with a horrible marketing message. It markets itself as a “fee free” banking alternative but the truth is its a little more complicated than that.

You see, Simple’s business model is that..well..of a bank. This particular bank makes money by providing profitable checking accounts which Simple markets as part savings account. However, any smart person knows that a checking account should never house any money outside of $$ for immediate expenses for that month.

So then why does Simple encourages you to save inside of a checking account using such its “goals” feature among others? Because if this message works, you can easily see people reaching a $10k or more balance in their checking account.

Whether this is $2,000 for an emergency fund, $5,000 you were saving for a car, a $2k buffer fund for the year etc, the person who keeps that type of money at Simple is losing $20 – $150 or more per year by not keeping it in a typical online savings account. (Think Capital One).

That, my friends, is a fee.

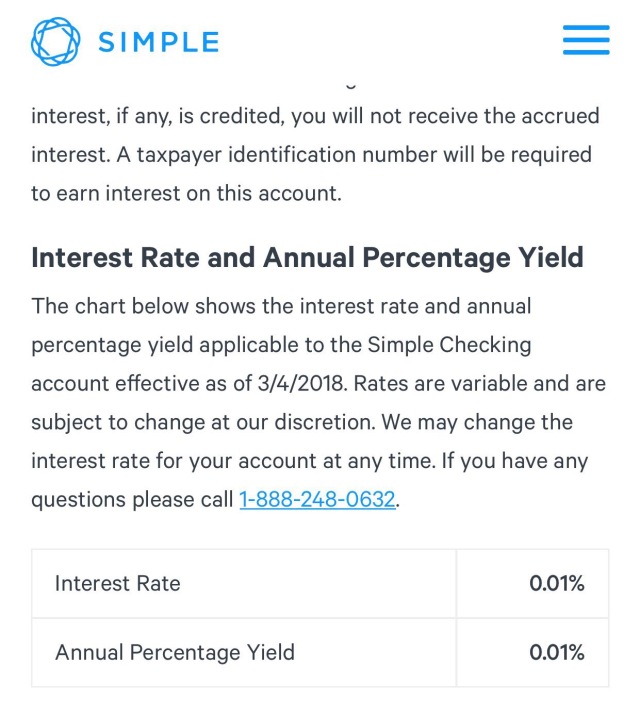

Simple then splits the amount it makes from making loans against this collateral with their network of banks. As a matter of fact, with a checking account paying only .001% APY, it appears Simple splits the profits earned on your money with everyone but…you.

Oh wait..they did give you a “fee free” bank account in exchange. 😂

FYI- Capital One 360, Chime bank and Ally Bank all offer a similar checking account product but with standard marketing

But can you incur fees? Every bank account has a potential to trigger fees. The only question is how well they’re hidden.

Now you know.